Home

Home- COVID-19

- Members

- MLS Tools

- AA Public Schools - Attendance Area by Street directory

- Area Housing Stats

- CBOR & CPIX Alliance

- Coming Soon Status

- Guest Listings

- MLS Compensation Codes

- MLS Rules & Regulations

- MLS Updates & Tips

- Property Profile Sheets

- Property Tax Links

- REALTOR® Property Resource (RPR)

- ShowingTime

- Washtenaw County & RealComp Map Areas

- ZipForm Online

- Zoning Resources

- Resources

- Calendar

- Buy & Sell

- Contact Us

- About

New condominium listings saw a significant 12.8% increase along with condominium sales rising by 27.9%.

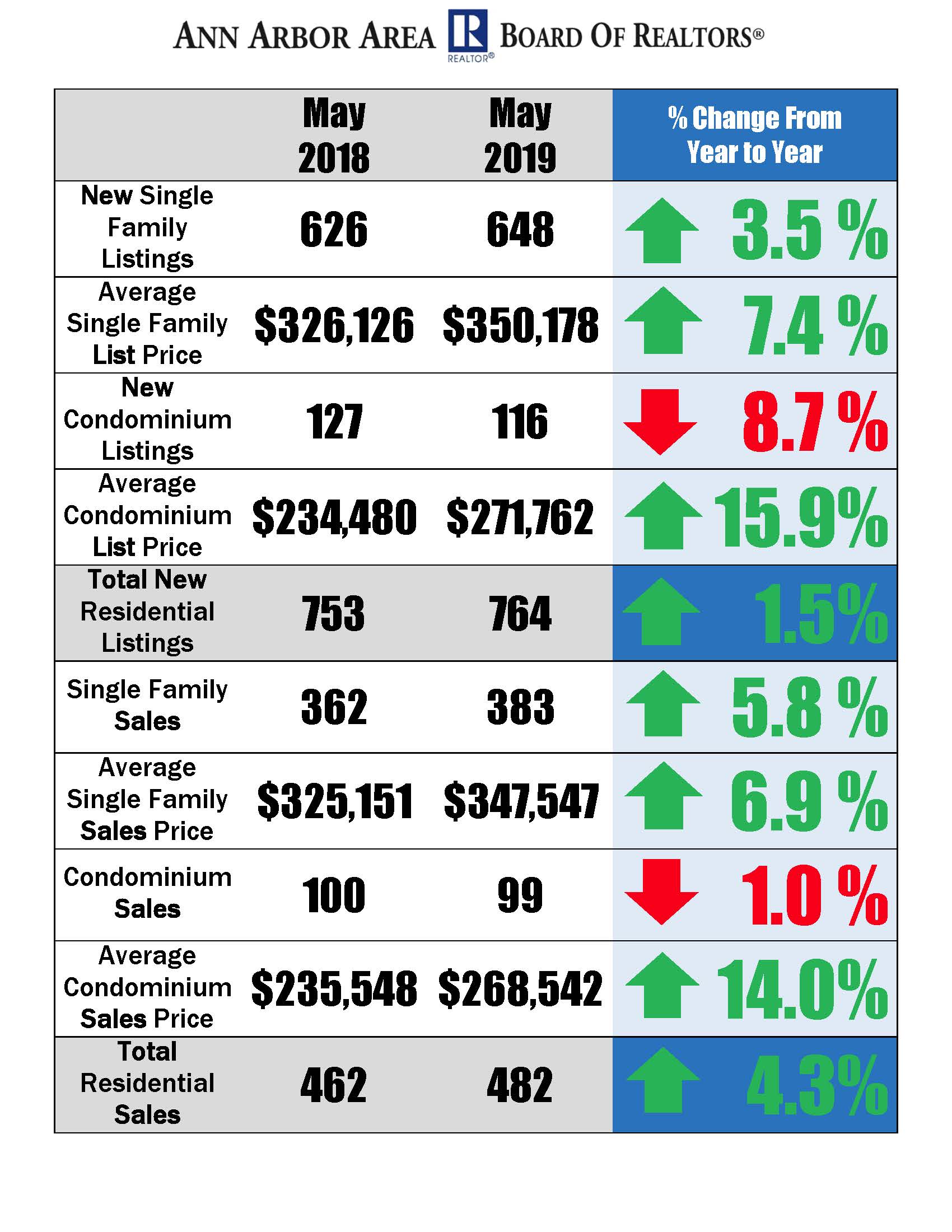

New single family listings increased in May, with a 3.5% rise compared to this time last year. Along with the growth in single family listings, the average listing price improved by 7.4%. The overall sales of single family listings increased by 5.8% compared to 2018 at this time.

New condominium listings saw an 8.7% decrease along with condominium sales falling by 1%. However, the average condominium list price rose 15.9% and sales prices increased 14% compared to that of 2018. During this past May, we saw 99 condominiums sell and a total of 482 residential sales compared to May 2018.

Year-to-date, the total number of new residential listings compared to 2018 rose 1.5% and total residential sales increased by 4.3% compared to May of 2018.

Inventory continued to increase in March, with a 9.7% increase in new single family listings compared to this time last year, and a 25.7% increase in new condominium listings.

As the bitter cold and drastic weather rolled in, the January 2019 Ann Arbor are housing market froze.

Overall, the Ann Arbor area housing market saw higher housing prices in 2018 compared to 2017.